Ultra Market Research | Fallopian Tube Cancer Market

Fallopian Tube Cancer Market

Report ID : 1194

Category : Therapeutic-Area

No Of Pages : 99

Published on: August 2025

Status: Published

Format :

Key Question Answer

Global Market Outlook

In-depth analysis of global and regional trends

Analyze and identify the major players in the market, their market share, key developments, etc.

To understand the capability of the major players based on products offered, financials, and strategies.

Identify disrupting products, companies, and trends.

To identify opportunities in the market.

Analyze the regional penetration of players, products, and services in the market.

Comparison of major players financial performance.

Evaluate strategies adopted by major players.

Recommendations

Fallopian Tube Cancer Market

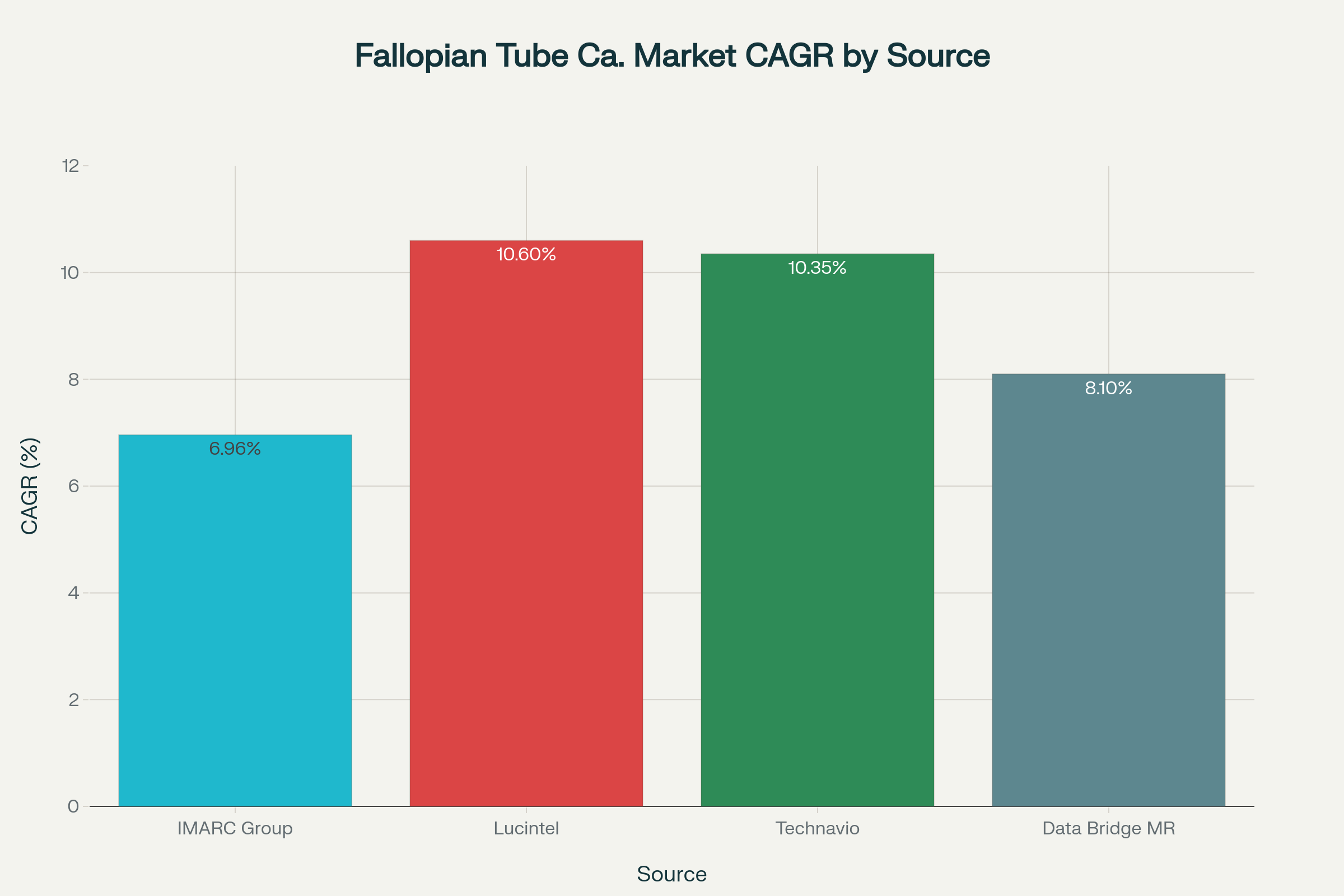

The global fallopian tube cancer market represents a specialized but increasingly significant segment within gynecological oncology, driven by evolving diagnostic practices and therapeutic innovations. This rare malignancy, which affects the fallopian tubes connecting the ovaries to the uterus, has gained heightened attention as research reveals its connection to high-grade serous ovarian carcinomas. The market is experiencing robust growth with multiple forecasts indicating strong compound annual growth rates (CAGR) ranging from 6.96% to 10.6% through 2034. This expansion reflects not only increased disease recognition but also significant advances in targeted therapies, immunotherapy approaches, and precision medicine applications that are transforming treatment paradigms for patients with this challenging condition. Globally, fallopian tube cancer accounts for approximately 1,500 to 2,000 reported cases worldwide, with the United States seeing approximately 300 to 400 new diagnoses annually. Despite its rarity, the market's economic impact extends beyond direct treatment costs, encompassing research and development investments, healthcare infrastructure improvements, and the broader implications for gynecological cancer management strategies.

Market Segmentation

By Product Type

Targeted Therapy Segment The targeted therapy segment dominates the fallopian tube cancer therapeutics market, representing the fastest-growing treatment modality. This segment includes PARP inhibitors such as olaparib (Lynparza), niraparib (Zejula), and rucaparib, which have shown particular efficacy in patients with BRCA mutations. Targeted therapies are expected to witness higher growth due to their ability to inhibit specific cancer-causing genes, proteins, or cellular pathways.

Chemotherapy Segment Traditional chemotherapy remains a cornerstone of fallopian tube cancer treatment, typically involving platinum-based regimens combined with taxanes. While facing competition from newer targeted approaches, chemotherapy continues to play a vital role in combination therapies and as first-line treatment for many patients.

By Application

Hospitals Segment Hospitals constitute the largest end-user segment, accounting for approximately 66% of healthcare facilities planning comprehensive business model overhauls for oncology services10. The hospital pharmacy segment held the largest revenue share at around 46% in 2024, driven by the primary role hospitals play in cancer diagnosis, treatment, and patient management.

Clinics and Ambulatory Surgery Centers This segment represents a growing portion of the market as healthcare delivery shifts toward specialized outpatient facilities. Clinics and ASCs offer advantages in terms of cost efficiency and patient convenience for certain procedures and follow-up care.

Online Pharmacy Segment The online pharmacy segment is projected to register the fastest CAGR of 8.1% during the forecast period, reflecting broader digitalization trends in healthcare and improved patient access to specialized medications.

By Region

North America North America dominates the global fallopian tube cancer market with the largest revenue share of 44% in 2024. The region benefits from advanced healthcare infrastructure, high R&D spending, and strong regulatory frameworks that facilitate rapid adoption of innovative therapies. The United States alone accounts for a significant portion of this market, with robust clinical trial activities and leading pharmaceutical companies.

Europe Europe represents the second-largest market for fallopian tube cancer therapeutics, characterized by established healthcare systems and strong regulatory oversight13. Countries like the United Kingdom, Germany, and France contribute significantly to market growth through research initiatives and comprehensive cancer care programs.

Asia-Pacific The Asia-Pacific region is expected to experience the fastest growth rate of 8.0% during the forecast period. This growth is driven by large patient populations, rising healthcare expenditure, improving diagnostic capabilities, and increasing awareness of gynecological cancers. China, India, and Japan are key contributors to regional market expansion.

Latin America and Middle East & Africa These regions represent emerging markets with moderate growth potential, driven by improving healthcare access, growing awareness of women's health issues, and increasing healthcare investments.

Key Market Players

The fallopian tube cancer therapeutics market features a competitive landscape dominated by established pharmaceutical giants and emerging biotech companies. The following table highlights the top companies driving market innovation:

Company

Headquarters

Key Products/Focus

AbbVie Inc.

United States

PARP inhibitors, Oncology therapies

AstraZeneca

United Kingdom

Targeted therapies, Immunotherapy

Bristol Myers Squibb

United States

Immunotherapy, Checkpoint inhibitors

Eli Lilly and Company

United States

Targeted therapies, Oncology

F. Hoffmann-La Roche Ltd.

Switzerland

Targeted therapies, Diagnostics

GlaxoSmithKline plc

United Kingdom

PARP inhibitors, Immunotherapy

Johnson & Johnson

United States

Comprehensive oncology portfolio

Merck & Co. Inc.

United States

PARP inhibitors, Immunotherapy

Novartis AG

Switzerland

Targeted therapies, Oncology

Pfizer Inc.

United States

Comprehensive cancer treatments

Strategic Developments

Mergers and Acquisitions The market has witnessed significant M&A activity as companies seek to strengthen their oncology portfolios. Notable transactions include licensing agreements for novel drug candidates and strategic partnerships for clinical development programs.

New Product Launches Recent FDA approvals have reshaped the treatment landscape, including Elahere (mirvetuximab soravtansine-gynx) for platinum-resistant ovarian cancer15, which also applies to fallopian tube cancer patients. GSK's dostarlimab in combination with niraparib has shown promising results in the FIRST trial.

Partnerships and Collaborations Companies are increasingly forming strategic alliances to accelerate drug development. Notable partnerships include collaborations between pharmaceutical companies and academic institutions for clinical trials and biomarker development.

Market Drivers

Rising Disease Incidence and Awareness The increasing recognition of fallopian tube cancer as a distinct clinical entity has led to improved diagnostic practices and treatment protocols.Growing awareness campaigns and educational initiatives by organizations like the Foundation for Women's Cancer have enhanced early detection rates.

Genetic Testing Expansion The widespread adoption of BRCA1/2 genetic testing has identified more high-risk patients, leading to increased demand for targeted therapies and preventive measures1920. Approximately 80% of high-grade serous epithelial ovarian cancers, which often originate in the fallopian tubes, have tumors that overexpress folate receptor-alpha (FR-α).

Technological Advancements Innovations in molecular profiling, precision medicine, and biomarker identification have enabled more personalized treatment approaches218. The development of companion diagnostics and liquid biopsies has improved patient stratification and treatment selection.

Immunotherapy Advances The integration of immune checkpoint inhibitors into treatment regimens represents a paradigm shift in fallopian tube cancer management2122. Combinations of immunotherapy with targeted therapies are showing promising results in clinical trials.

PARP Inhibitor Evolution Next-generation PARP inhibitors with improved selectivity and reduced toxicity profiles are entering clinical development8. Selective PARP1 inhibitors like AZD5305 aim to minimize myeloid neoplasia risks associated with current PARP inhibitors.

Antibody Drug Conjugates ADCs targeting folate receptor-alpha, such as Elahere, represent a significant advancement in targeted delivery of cytotoxic agents specifically to cancer cells.

Market Restraints

High Treatment Costs The expensive nature of advanced cancer therapies and prolonged treatment regimens limits patient access and healthcare system adoption, particularly in resource-constrained settings25. Novel targeted therapies and immunotherapies often carry premium pricing that challenges healthcare budgets.

Late-Stage Diagnosis Challenges The asymptomatic nature of early-stage fallopian tube cancer leads to delayed detection, reducing treatment efficacy and patient survival outcomes. The lack of effective screening methods for this rare cancer contributes to diagnostic delays.

Limited Treatment Response Rates Drug resistance development and variable patient responses to existing therapies constrain treatment success rates and market expansion25. The heterogeneity of fallopian tube cancer complicates the development of universal treatment protocols.

Complex Approval Processes Stringent drug approval processes and clinical trial requirements delay the introduction of new therapeutic options to the market. The rarity of fallopian tube cancer makes it challenging to conduct large-scale clinical trials necessary for regulatory approval.

Healthcare Access Disparities Geographic and socioeconomic barriers to specialized cancer care limit market penetration in underserved populations and developing regions25. The concentration of expertise in major medical centers creates access challenges for patients in rural areas.

Opportunities & Future Trends

Precision Medicine Expansion The growing emphasis on personalized medicine creates significant opportunities for tailored therapies based on individual patient genetic profiles926. Genomic profiling and biomarker-driven treatment selection represent key growth areas.

Combination Therapy Development The development of novel combination regimens involving targeted therapies, immunotherapy, and traditional chemotherapy offers potential for improved patient outcomes827. Clinical trials exploring synergistic combinations are showing promising preliminary results.

Digital Health Integration The expansion of telemedicine and remote monitoring solutions presents opportunities for improved patient care and follow-up, particularly highlighted by the COVID-19 pandemic's impact on healthcare delivery.

Predicted Consumer Behavior and Innovations

Patient-Centric Care Models Healthcare systems are increasingly adopting patient-centric approaches that emphasize quality of life, personalized treatment plans, and comprehensive support services. This trend is driving demand for more targeted and less toxic treatment options.

Early Detection Technologies Investment in liquid biopsy technologies and advanced imaging modalities for early detection represents a significant market opportunity29. These technologies could transform the treatment landscape by enabling intervention at earlier disease stages.

Biomarker-Driven Therapy Selection The future of fallopian tube cancer treatment lies in biomarker-driven therapy selection, with companion diagnostics playing an increasingly important role in treatment decision-making.

Regional Insights

North America Market Dynamics North America maintains its position as the dominant market with advanced healthcare infrastructure and high R&D investments1312. The region benefits from rapid adoption of innovative therapies and strong reimbursement frameworks. The United States alone represents a significant portion of the global market, with an estimated 300-400 new fallopian tube cancer cases diagnosed annually.

European Market Characteristics Europe represents a mature market with established healthcare systems and comprehensive cancer care programs13. The region's strong regulatory framework and emphasis on evidence-based medicine drive consistent market growth. Key markets include the United Kingdom, Germany, France, and the Nordic countries.

Asia-Pacific Growth Trajectory The Asia-Pacific region demonstrates the highest growth potential, driven by large patient populations, improving healthcare infrastructure, and rising healthcare expenditure. Countries like China, India, and Japan are experiencing increased cancer incidence rates and improved access to advanced therapies.

Market Size and Forecast by Geography

The following table summarizes regional market characteristics and growth drivers:

Region

Market Position

Key Drivers

North America

Largest market share

Advanced healthcare infrastructure, High R&D spending

Europe

Second largest market

Strong regulatory framework, Established healthcare systems

Asia-Pacific

Fastest growing region

Large patient population, Rising healthcare expenditure

Latin America

Moderate growth

Improving healthcare access, Growing awareness

Middle East & Africa

Emerging market

Increasing healthcare investments, Rising cancer incidence

Key Insights

The global fallopian tube cancer market represents a dynamic and rapidly evolving sector within gynecological oncology, characterized by robust growth projections and significant therapeutic innovations. With CAGR estimates ranging from 6.96% to 10.6% through 2034, the market reflects the successful integration of precision medicine approaches, targeted therapies, and improved diagnostic practices.The market's transformation is driven by several key factors: the recognition of fallopian tube cancer's relationship to high-grade serous ovarian carcinomas, advances in genetic testing and biomarker identification, and the development of novel therapeutic approaches including PARP inhibitors, immunotherapy, and antibody-drug conjugates. These developments have created new treatment paradigms that offer improved patient outcomes and quality of life.Regional analysis reveals North America's continued dominance, while Asia-Pacific emerges as the fastest-growing market segment, presenting significant opportunities for market expansion and investment. The competitive landscape features established pharmaceutical giants alongside innovative biotech companies, all competing to address the unmet medical needs in this specialized therapeutic area.

Strategic Recommendations for Stakeholders

For Pharmaceutical Companies:

Invest in biomarker-driven drug development programs focusing on genetic mutations and molecular targets specific to fallopian tube cancer. Develop strategic. partnerships with diagnostic companies to create companion diagnostic tests Expand clinical trial networks to include diverse patient populations and geographic regions. Focus on combination therapy development to overcome resistance mechanisms and improve efficacy

For Healthcare Providers:

Implement comprehensive genetic testing protocols for high-risk patients. Establish multidisciplinary care teams specialized in gynecological oncology. Invest in advanced diagnostic technologies and molecular profiling capabilities. Develop patient education programs to improve awareness and early detection

For Investors:

Consider opportunities in companies developing next-generation PARP inhibitors and immunotherapy combinations. Evaluate investments in digital health. platforms focusing on cancer care and remote monitoring. Assess biotechnology companies with novel approaches to drug delivery and targeted therapy. Monitor regulatory developments and reimbursement policies that could impact market access

For Policymakers:

Support initiatives to improve access to genetic testing and counseling services. Invest in research infrastructure and clinical trial networks. Develop frameworks for accelerated approval pathways for rare cancer therapeutics. Promote international collaboration in rare disease research and drug development. The fallopian tube cancer market's future success will depend on continued innovation, improved patient access to advanced therapies, and the development of more effective early detection methods. As our understanding of this disease's molecular biology advances, the market is well-positioned for sustained growth and the delivery of meaningful therapeutic benefits to patients worldwide.

Market research reports estimate the global fallopian tube cancer therapeutics market will grow at a CAGR of approximately 7%–10.6% from 2024 to 2034, with incremental market expansions ranging from USD 628 million to USD 832 million over various forecast periods.

The targeted therapy segment—including PARP inhibitors and antibody-drug conjugates—holds the largest share and is the fastest-growing modality, driven by precision-medicine advances and improved patient outcomes.

Top players include AbbVie Inc., AstraZeneca, Bristol Myers Squibb, Eli Lilly, Roche, GSK, Johnson & Johnson, Merck, Novartis, and Pfizer. These companies lead through proprietary oncology pipelines, strategic partnerships, and recent product launches such as Elahere.

Key drivers include rising fallopian tube cancer awareness, expansion of BRCA genetic testing, innovations in targeted therapies and immunotherapies, and the development of companion diagnostics for personalized treatment.

High treatment costs, delayed diagnosis due to asymptomatic early stages, variable patient response and resistance to therapies, and stringent regulatory requirements for rare cancer drug approvals pose significant market restraints.

2

3

Market Segmentation

By Product Type

Targeted Therapy Segment The targeted therapy segment dominates the fallopian tube cancer therapeutics market, representing the fastest-growing treatment modality. This segment includes PARP inhibitors such as olaparib (Lynparza), niraparib (Zejula), and rucaparib, which have shown particular efficacy in patients with BRCA mutations. Targeted therapies are expected to witness higher growth due to their ability to inhibit specific cancer-causing genes, proteins, or cellular pathways.

Chemotherapy Segment Traditional chemotherapy remains a cornerstone of fallopian tube cancer treatment, typically involving platinum-based regimens combined with taxanes. While facing competition from newer targeted approaches, chemotherapy continues to play a vital role in combination therapies and as first-line treatment for many patients.

By Application

Hospitals Segment Hospitals constitute the largest end-user segment, accounting for approximately 66% of healthcare facilities planning comprehensive business model overhauls for oncology services10. The hospital pharmacy segment held the largest revenue share at around 46% in 2024, driven by the primary role hospitals play in cancer diagnosis, treatment, and patient management.

Clinics and Ambulatory Surgery Centers This segment represents a growing portion of the market as healthcare delivery shifts toward specialized outpatient facilities. Clinics and ASCs offer advantages in terms of cost efficiency and patient convenience for certain procedures and follow-up care.

Online Pharmacy Segment The online pharmacy segment is projected to register the fastest CAGR of 8.1% during the forecast period, reflecting broader digitalization trends in healthcare and improved patient access to specialized medications.

By Region

North America North America dominates the global fallopian tube cancer market with the largest revenue share of 44% in 2024. The region benefits from advanced healthcare infrastructure, high R&D spending, and strong regulatory frameworks that facilitate rapid adoption of innovative therapies. The United States alone accounts for a significant portion of this market, with robust clinical trial activities and leading pharmaceutical companies.

Europe Europe represents the second-largest market for fallopian tube cancer therapeutics, characterized by established healthcare systems and strong regulatory oversight13. Countries like the United Kingdom, Germany, and France contribute significantly to market growth through research initiatives and comprehensive cancer care programs.

Asia-Pacific The Asia-Pacific region is expected to experience the fastest growth rate of 8.0% during the forecast period. This growth is driven by large patient populations, rising healthcare expenditure, improving diagnostic capabilities, and increasing awareness of gynecological cancers. China, India, and Japan are key contributors to regional market expansion.

Latin America and Middle East & Africa These regions represent emerging markets with moderate growth potential, driven by improving healthcare access, growing awareness of women's health issues, and increasing healthcare investments.